For many Australians affected by the Shield Master Fund and First Guardian collapse, receiving a payment from Macquarie into a Cash Management Account (CMA) felt like the end of a long and stressful journey.

After months of uncertainty, many people understandably thought, “Finally, my money is back.”

Some assumed the money had automatically been returned to their superannuation account. Others left it sitting in the CMA, believing the platform would eventually move it somewhere on their behalf. Some withdrew the funds to cover everyday expenses or make purchases, while many simply weren’t sure what they should do next.

The reality is that thousands of Australians have suddenly found themselves responsible for making an important financial decision, often without fully understanding why the money was paid into a CMA, how it is treated for tax and superannuation purposes, or what opportunities it may create.

While every person’s circumstances are different, the arrival of these funds may provide a rare opportunity to strengthen your financial position, reduce debt, improve retirement savings, or create greater financial security for the future.

Before making any decisions, it is worth understanding exactly what a CMA payment is, where the money sits, and the options available to you.

What should I do with it now? Should I just leave it in CMA?

The temptation is often to leave the money where it is until a decision becomes clearer.

Unfortunately, that can sometimes be the most expensive decision of all.

What many people don’t realise is that cash sitting idle often loses purchasing power over time through inflation and may also represent missed opportunities to reduce debt, improve cash flow or strengthen retirement savings.

The good news is that there does not need to be a single “right” answer.

In many cases, the most effective strategy involves sequencing several decisions together rather than choosing just one option.

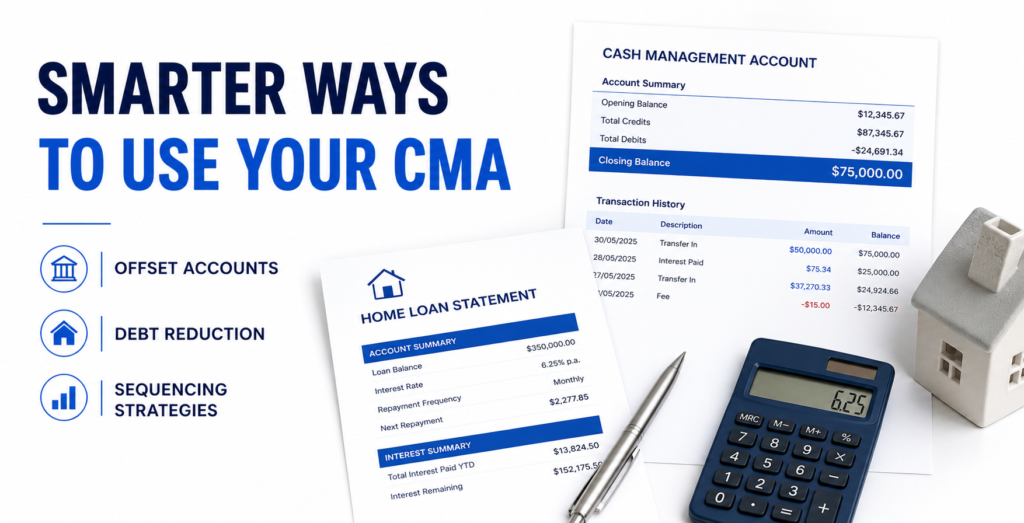

Let’s explore some of the smarter ways Australians may think about using money held in a CMA.

Why cash sitting still can cost more than you think

A CMA is designed primarily as a transaction and settlement account.

While it generally earns interest, the return is often lower than what may be available elsewhere.

Imagine Susan, aged 58, has $80,000 sitting in her CMA earning 2.5% interest.

Over one year she earns:

$80,000 × 2.5% = $2,000

After tax, her actual benefit may be significantly lower.

Meanwhile, if Susan has a home loan charging 6.5% interest, every dollar sitting in the CMA is effectively costing her money.

This is where understanding opportunity cost becomes important.

Opportunity cost simply means considering what else the money could be doing.

The question is not:

” How much is my CMA earning?”

The better question is:

” Could this money be working harder elsewhere?”

One of the simplest strategies available to homeowners is using an offset account.

An offset account is linked to a mortgage. The balance in the account reduces the amount of the loan on which interest is calculated.

Let’s look at a simple example.

David, aged 45, still owes $300,000 on his home loan.

Interest rate: 6.5%

CMA balance: $100,000

If David transfers the CMA funds into his offset account, interest is only calculated on:

$300,000 – $100,000 = $200,000

Annual interest saving:

$100,000 × 6.5% = $6,500

This saving is effectively tax-free because it comes from avoiding interest rather than earning taxable income.

To generate the same after-tax benefit from a bank account, David may need to earn considerably more than $6,500 depending on his marginal tax rate.

This is why offset accounts are often one of the most efficient uses of surplus cash.

Investments can rise and fall.

Interest savings from debt reduction are far more predictable.

Many Australians approaching retirement are carrying: • Home loans | • Investment loans | • Personal loans | • Car finance

Reducing debt can improve cash flow immediately.

Consider Jenny and Mark, both 57.

They have:

• Mortgage balance: $220,000

• Interest rate: 6.2%

• CMA balance: $70,000

If they use the full amount to reduce their mortgage:

$70,000 × 6.2%

Annual interest saving = $4,340

Over ten years, assuming rates remain similar, the cumulative savings become significant.

What makes debt reduction particularly attractive before retirement is that it lowers the income required to maintain lifestyle once employment income stops.

Many retirees discover that reducing expenses can be just as powerful as increasing investment returns.

A practical example might look like this:

Step 1

r

Step 2

Step 3

Step 4

Step 5

Step 6

Sequencing strategies

Many people assume they must choose between:

• Paying debt

• Investing

• Contributing to super

In reality, these strategies can often work together.

This is where sequencing becomes valuable.

Sequencing simply means using the same dollars in multiple ways over time.

Rather than making a single decision, the money continues working through different stages.

This approach has been discussed widely in relation to strategic use of CMA funds and tax planning opportunities for eligible Australians. The key concept is that tax refunds themselves can become part of a broader wealth-building process rather than simply being spent.

A case study: using multiple strategies together

The following example is hypothetical and for educational purposes only. Andrew is 56. He receives $120,000 into his CMA. Current situation: Mortgage balance: $350,000 | Mortgage rate: 6.5% | Income: $150,000 | Super balance: $420,000 Instead of leaving the money in cash, Andrew decides to create a staged strategy.

Stage 1

He contributes $40,000 to super and claims a tax deduction, subject to contribution rules and available caps.

Stage 2

After lodging his tax return, he receives a significant tax benefit.

Stage Three

Rather than spending the refund, he places it into his offset account.

Assume refund available for offset:

$13,850

Mortgage interest saving:

$13,850 × 6.5%

= approximately $900 per year

Stage 3

The remaining CMA funds stay available as a cash reserve while he reviews future opportunities.

Instead of making one decision, Andrew has:

• Increased retirement savings

• Improved tax efficiency

• Reduced mortgage interest

• Maintained liquidity

That is the power of sequencing.

What About Retirement?

For Australians over 50, retirement planning should always form part of the conversation.

Many people focus solely on investment returns.

However, retirement outcomes are often driven by:

• Tax efficiency

• Cash flow

• Debt levels

• Asset structure

• Timing decisions

A person entering retirement with no mortgage may require significantly less income than someone carrying debt.

This is why reducing liabilities before retirement can sometimes deliver a greater lifestyle benefit than chasing higher investment returns.

What many people don’t realise is that retirement planning is often less about maximising returns and more about optimising the structure of your finances.

Maintain Flexibility

While superannuation can offer attractive tax treatment, money contributed to super is generally preserved until a condition of release is met.

That means flexibility matters.

Many people approaching retirement benefit from maintaining a balance between:

• Accessible cash reserves

• Debt reduction

• Superannuation savings

• Other investments

A healthy emergency fund can prevent the need to access investments at the wrong time or accumulate additional debt when unexpected expenses arise.

Financial resilience is often just as important as investment growth.

The Bottom Line

Receiving money into a CMA is not necessarily a problem to solve.

It is an opportunity to think strategically.

For Australians some of the most effective uses of CMA funds may include:

- Reducing mortgage interest through an offset account

- Paying down non-deductible debt

- Improving retirement readiness

- Using tax deductions strategically

- Reinvesting tax refunds

- Creating a long-term sequencing strategy

The most important point is that cash rarely has to perform just one role.

With careful planning, the same pool of money may help improve tax outcomes, reduce interest costs, strengthen retirement savings and improve cash flow over time.

Sometimes the smartest strategy isn’t choosing one option. It’s choosing the order in which you use them.

General Information Warning

This article contains general information only and does not take into account your personal objectives, financial situation or needs. Before acting on any strategy, consider whether it is appropriate for your circumstances and seek professional advice. Superannuation, taxation and retirement planning rules are complex and subject to change. Past performance is not a reliable indicator of future performance.

External links