Most Australians don’t spend much time thinking about superannuation. For many people, it simply sits in the background while life moves on — work, mortgages, school fees, groceries, holidays and trying to get ahead. But from 1 July 2026, several major superannuation changes are coming into effect across Australia. Some of these changes could positively impact retirement savings, while others may create additional pressure for businesses and higher-income Australians. The challenge is that superannuation language can become very technical very quickly. So instead of using confusing financial jargon, let’s break down what is actually changing, why it matters, and what everyday Australians should realistically pay

Payday super

Real-life case

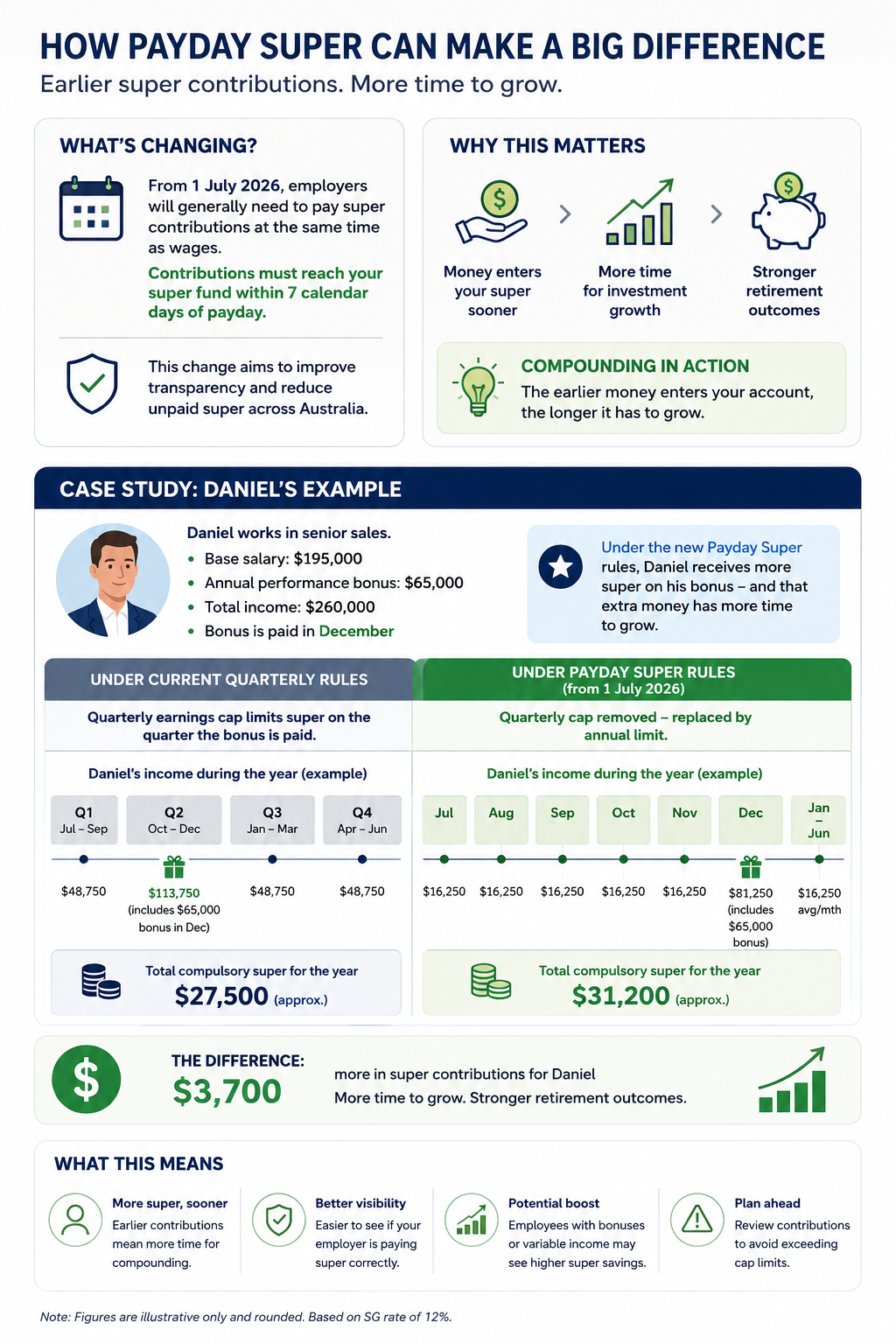

The most significant change is something called Payday Super.

At the moment, most employers pay superannuation quarterly. This means your employer may only transfer your super contributions four times per year.

From 1 July 2026, employers will generally need to pay super contributions at the same time as wages. Contributions must reach employees’ super funds within seven calendar days of payday.

This change has been introduced by the Australian Government to improve transparency and reduce unpaid superannuation across Australia.

According to the Australian Taxation Office, billions of dollars in superannuation have historically been paid late or missed entirely by employers.

Why this matters more than people realise?

At first glance, this might sound like an administrative change only affecting payroll teams.

But in reality, it could make a meaningful difference to long-term retirement balances.

Superannuation grows through compound earnings.

That simply means:

• money earns returns,

• then those returns also begin earning returns.

The earlier money enters a super account, the longer it has to compound.

Even small delays repeated over 30 or 40 years can reduce retirement balances more than people expect.

REAL CASE 1

Sarah is 36 and works in marketing.

She earns around $98,000 per year and rarely checked her super account because she assumed everything was being handled correctly.

A few years ago, she changed jobs and discovered one employer had been consistently paying her super late.

The employer eventually paid the missing contributions, but Sarah realised something important:

• She didn’t only lose access to the money temporarily.

• She also lost years of investment growth that money could have generated.

That is the hidden impact many Australians never see.

Under the new Payday Super system, situations like this should become much easier to identify much earlier.

REAL CASE 2

The changes may also be particularly important for employees who receive bonuses, commissions or variable income throughout the year. Under the current rules, employers only need to pay compulsory super up to a quarterly earnings limit. This has meant that some Australians receiving large bonuses may not have received super contributions on the full amount of those bonuses.

From 1 July 2026, this quarterly limit will effectively be replaced by an annual limit instead.

Daniel works in senior sales and earns: Base salary: $195,000, Annual performance bonus: $65,000, Total income: $260,000

His annual bonus is paid in December each year.

Under the current quarterly super rules, Daniel’s employer would only be required to contribute approximately: $27,500 into super for the year.

Under the new Payday Super rules, that quarterly limit no longer applies in the same way. As a result, his employer would contribute approximately: $31,200 into super for the year.

The difference: Daniel receives approximately $3,700 more in super contributions

Importantly, that extra money now has additional years to remain invested and compound within super.

For employees receiving: bonuses, commissions, overtime, or fluctuating income, these changes could potentially improve long-term retirement balances over time

However, it may also increase the risk of exceeding concessional contribution caps, particularly for people already salary sacrificing into super. This is why reviewing contribution strategies before July 2026 may become increasingly important.

The new tax on super balances above $3 million

Another major change beginning from 1 July 2026 is the introduction of an additional tax on very large superannuation balances.

Individuals with total super balances exceeding $3 million may pay an additional 15% tax on earnings linked to the portion above that threshold.

This proposal has created significant debate across Australia because part of the calculation may include unrealised gains.

Unrealised gains are increases in asset value that have not actually been sold yet.

For example:

• if shares or property inside super increase in value,

• tax may potentially apply even if the investment has not been sold.

Will this affect most Australians?

No.

For most Australians, this will not have a direct impact.

However, it does highlight something important:

Superannuation rules can and do change regularly.

That is why retirement planning should never rely on assuming today’s rules will stay identical forever.

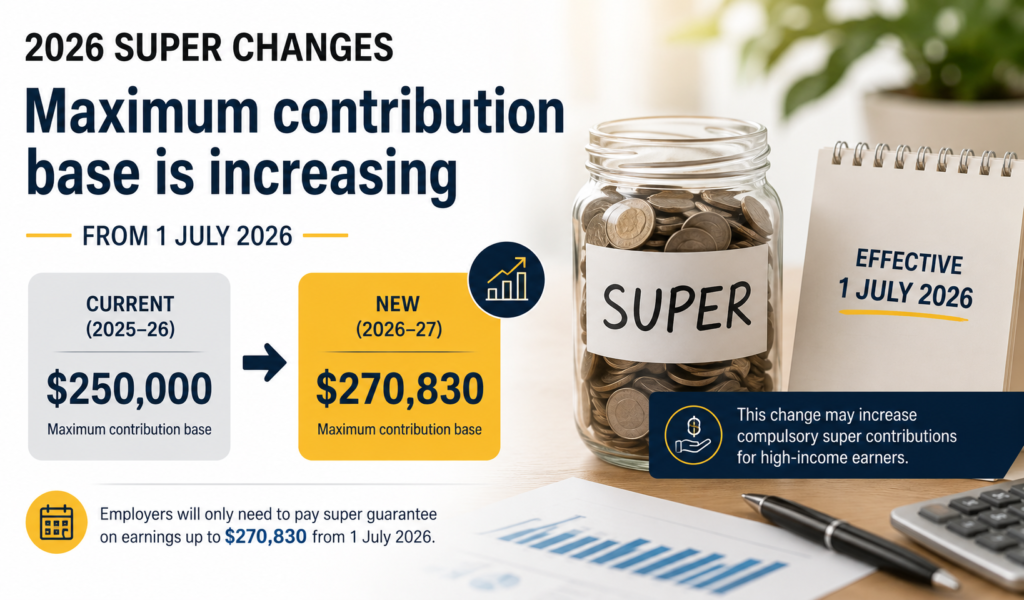

The maximum contribution base is increasing

From 1 July 2026, the maximum contribution base will increase to $270,830.

This is the maximum salary amount employers are required to use when calculating compulsory Super Guarantee contributions.

In simple terms

If someone earns above this amount:

• employers are generally not required to pay compulsory super contributions on income above the threshold.

This mainly affects higher-income earners.

Small business owners may feel the most pressure

Retirement benchmarks are also changing

While employees will likely welcome Payday Super, many small businesses may face additional cash flow pressure.

Previously, businesses could:

• hold super payments,

• manage them quarterly,

• and release them later.

Now, super payments will need to happen far more regularly.

For businesses already operating with tight margins, this may require:

• better payroll systems,

• improved cash flow forecasting,

• stricter budgeting,

• and faster administration.

The ATO’s Small Business Superannuation Clearing House is also closing, meaning businesses will need to transition to alternative SuperStream-compliant payment systems.

Many Australians underestimate how much money may actually be needed in retirement.

Current retirement benchmarks often suggest approximately:

• around $630,000 ($595,000 in 2024) for a comfortable retirement for a single person,

• around $730,000 ($690,000 in 2024) for a couple.

Source: ASFA Retirement Standard

But “comfortable retirement” means different things to different people.

For some Australians, comfort means:

• overseas travel,

• helping children financially,

• dining out regularly,

• and maintaining an active lifestyle.

For others, comfort simply means:

• stability,

• reduced stress,

• and not worrying about bills each month.

That’s why retirement planning should never be purely about chasing the largest number possible.

It should be about creating a strategy that suits your actual life.

Final thoughts

One thing we regularly notice is that many Australians become overwhelmed by superannuation.

- Contribution caps change.

Tax rules change.

Pension rules change.

Governments introduce new legislation.

Eventually, some people stop engaging with their super completely because it feels too confusing. That is usually the worst outcome. Because even small decisions made consistently over time can create a very large difference later.

Simple habits matter:

- checking your super balance,

- reviewing fees,

- ensuring insurance is still appropriate,

- consolidating old accounts,

- reviewing investment options,

- and making additional contributions where suitable.

None of these things are particularly exciting. But they can significantly impact retirement outcomes over decades.

Sources:

- Australian Taxation Office – Payday Super

- Australian Taxation Office – Super Guarantee

- ASFA Retirement Standard